How Your Credit Score Influences Your Auto Loan Rate

[ad_1]

The most essential ingredient of an vehicle-loan is arguably the fascination price. It specifically influences the sizing of month-to-month payments and all round mortgage tenor. Fascination rates can even engage in a job in the remaining shopping for decision, strong adequate to override sentimental acquire good reasons these as manufacturer loyalty. It goes with no expressing, hence, that potential auto potential buyers shell out attention to things that ascertain their curiosity charges when shopping for automobile-financing alternatives.

1 of this sort of elements is the credit score score. It is essentially a weighted score that tells auto-loan providers how much chance they are getting on by working with a potential borrower. You most probable have a credit rating report if you have any credit history accounts, this sort of as credit rating playing cards, mortgages or financial loans. This report then varieties the foundation for identifying your credit rating.

It is not an precise measure, but it does drop light-weight on things these types of as the borrower’s willingness and potential to provider the personal loan. Simply set, the far better your credit score score, the larger your prospects of securing an vehicle bank loan with favourable fascination fees. This is notably critical right now as we navigate the era of curiosity level hikes and inflationary pressures.

Using your credit history rating to protected the finest desire charges

By means of Experian

The all round reason of the credit score rating is common. Even so, distinctive loan companies in different sections of the earth have their possess conditions to measure an individual’s creditworthiness. When you use for an vehicle financial loan in the US, the loan provider will run a credit history test as aspect of the approach. The greater part of the lending institutions use FICO credit history scores. This is a 3-digit rating assigned to a borrower soon after the credit score look at exercising.

It was at first designed in 1989 by a info analytics company called Good Isaac Business. Now, there are lots of versions of the FICO algorithm (and other scoring designs, for that matter), but they are all aimed at ascertaining the borrower’s capability to acquire on credit rating.

Via The Harmony

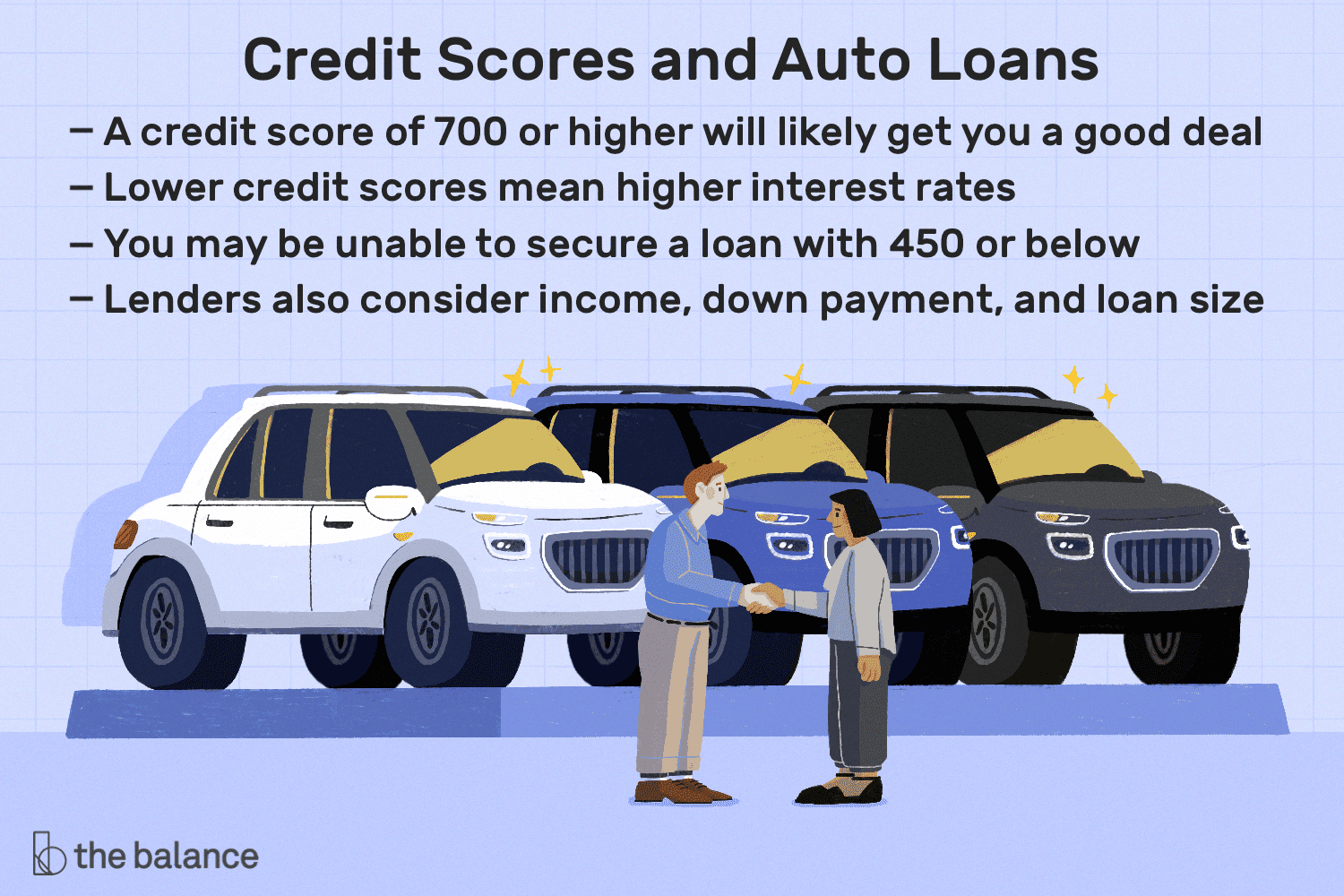

In accordance to the CFPB (Client Money Defense Bureau) Client Credit Panel, there are five different borrower profiles sorted into the pursuing credit rating rating buckets: Super-key (720 & over) Primary (660-719) In the vicinity of-primary (620-659) Subprime (580-619) Deep subprime (under 580). A borrower with a score down below 660 can nonetheless secure car financial loans, but they will be more pricey than a Prime or Super-primary borrower with a score north of 661. The logic here is that you will want to keep your credit score as large as feasible to get the finest discounts when browsing for automobile financial loans.

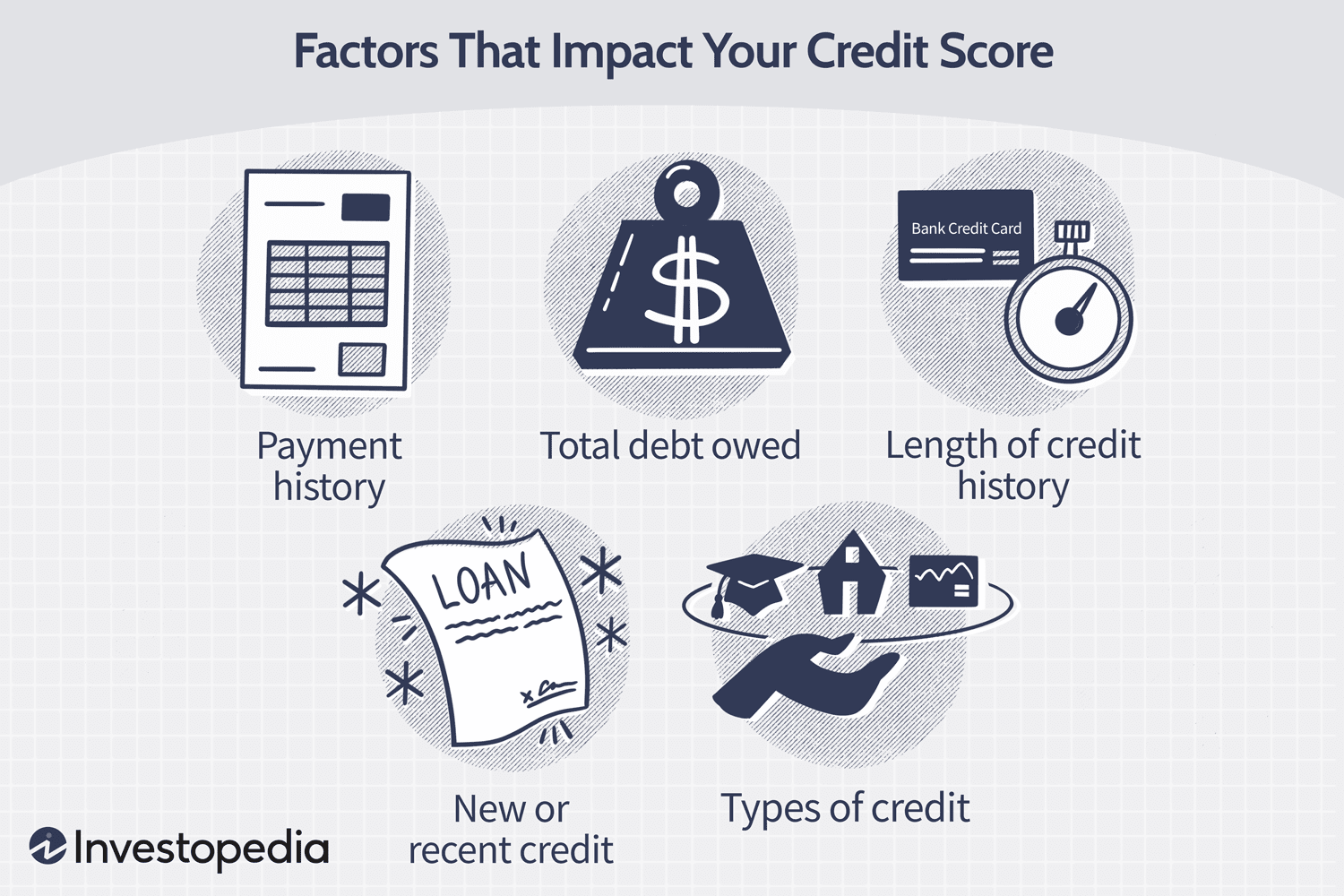

Issues that hurt your credit rating rating

Via Investopedia

An fantastic credit rating score is the consequence of very careful and deliberate setting up, and being aware of the potential pitfalls can aid the borrower avoid producing missteps that pull down the score into undesired territory.

Creating a late payment

Payment record on your credit score obligations accounts for up to 35% of the FICO rating. According to FICO, a payment that is 30 times late can charge a person with a credit score of 780 or better any place from 90 to 110 details. It is significant to make payments as at when due and proactively arrive at out to the loan company if, for any reason, payment will be delayed.

A high credit card debt-to-credit score utilization ratio

Credit score history is created by a continuous cycle of credit rating utilization and pay back downs. Nevertheless, you will want to preserve an eye on the proportion of your debt load to over-all credit. The reduce your balances relative to your full obtainable credit rating, the improved your score will be.

Non-utilization of credit history

On the other hand, no credit background for an extended period can also adversely have an impact on the borrower’s credit history rating. Creditors and creditors have nothing at all to report to credit bureaus when you don’t employ your credit rating accounts. This will make it a lot more challenging to examine potential personal loan programs.

Individual bankruptcy

Filing for bankruptcy has a single of the most substantial impacts on your credit history score. It can wipe as significantly as 240 factors from an individual’s rating, and what’s extra? A personal bankruptcy report can stay on the credit rating record for up to 10 decades.

This checklist is by no implies exhaustive, and other elements such as frequency of credit score applications, credit score card closure, demand-offs and refinancing all effect credit rating scores in varying levels.

Improving your credit rating score

Strengthening your credit history rating will entail averting the pitfalls before recognized higher than. Methods this kind of as prompt and standard bill payments, retaining a small credit card debt-to-credit utilization ratio (preferably about 30%), holding credit card accounts open and preventing a number of bank loan purposes at once are all ways in the proper course.

On the other hand, even with all these ‘building blocks’ in area, a wonderful credit score is not instantaneous. It may choose a although to see any enhancement, especially since adverse studies can keep on your credit heritage for a number of a long time. There is no rigid time body for credit rating rating growth as just about every person’s monetary circumstance is unique. In accordance to Forbes, it could choose wherever from a month to as a lot as 10 decades. Naturally, this is affected by variables these kinds of as the individual’s present-day credit history standing and sum of full exposure.

Securing car financial loans irrespective of credit score

Via Geotab

A significant credit score rating will definitely strengthen your chances of securing auto funding and locking up the finest curiosity charges. Nevertheless, it is not all doom-and-gloom for future car customers with weak scores as they are not entirely with no solutions.

Regardless of your credit history rating, hunting about and looking at the a variety of funding solutions is very encouraged. It is just like procuring for the vehicle by itself an ordinary buyer will assess different dealerships and negotiate vigorously in advance of building the closing decision.

Banking companies are the traditional sources for getting a loan, but you could be limiting your options if they are your only thought. Don’t ignore choice creditors. Doing work with 3rd-get together financing businesses, these as receiving your vehicle financial loan via LoanCenter.com, may provide you with favourable fascination rates or financing terms.

It is crucial to notice that just getting auto-financial loan preapprovals (different from precise financial loan programs) when shopping about will not effect your credit score because most scoring designs do not treat this as a tricky enquiry.

In summary, a weak credit rating score may press the cheapest desire prices out of attain. Nonetheless, getting a number of solutions will improve your possibilities of locating a package deal with an curiosity rate that suits within just your price range and permit you to invest in your wanted auto.

[ad_2]

Resource hyperlink